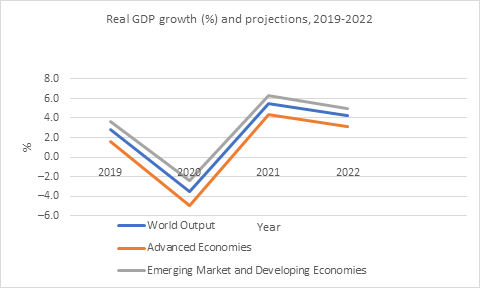

The latest (January 2021) IMF estimates reveal that world GDP for 2020 is expected to fall by 3.5 percent, with the advanced economies registering a projected decline of 4.9 percent. Emerging and developing economies are estimated to endure a fall in real GDP of 2.4 percent (Figure 1). This is unlike the last global recession of 2008 when the emerging and developing economies registered modest positive growth juxtaposed with a significant decline of more than 3 percent for the advanced economies. The net impact was that, at the global level, output contracted by a modest 0.1 percent.

Figure 1

Source: Derived from IMF, World Economic Outlook, January 2021

A ‘V’ shaped recovery is expected in 2021 across the world and the projections suggest that between 2020 and 2025 both the advanced and emerging and developing economies will continue to grow at a steady pace in line with recent historical trends (IMF data mapper, October 2020). Such a salutary outcome, however, rests on the critical assumption that appropriate policy responses across the world will be enacted and implemented and that the timely availability of vaccines will offer durable protection against the current pandemic. In the absence of appropriate policy interventions, much more pessimistic interpretations of the nature of the global economic recovery are very likely. This point is elucidated below.

A number of analysts have highlighted the notion that aggregate growth statistics hide the fact that a ‘K-shaped’ or uneven recovery is in progress.[1] This can be gauged from both sectoral growth and employment patterns and the nature of job losses across cohorts of workers stratified by income and skill levels.

The ILO’s latest Global Monitor (January 2021) notes that specific sectors, most notably, ‘accommodation and food services, arts and culture, retail, and construction’, have experienced massive job losses, while positive job growth is evident in information and communication, and financial and insurance activities which tend to be populated by higher skilled workers. Others find that the semiconductor industry is booming, while contact-intensive, service-oriented industries are languishing.[2]

Evidence from the USA highlights a striking pattern: high wage workers experienced job gains (+2.9 percent) during the pandemic, middle wage workers experienced modest job losses (-3.4 percent), while low wage workers experienced massive job losses (-21 percent).[3] This implies that COVID-19 is likely to exacerbate existing inequalities unless countervailing policy measures are undertaken.

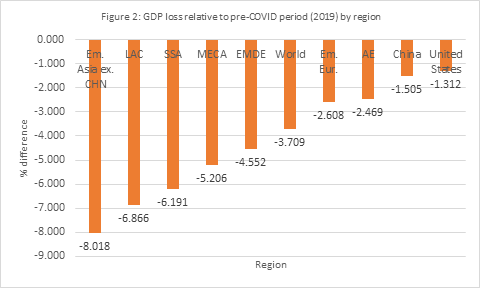

The thesis of uneven economic recovery also pertains to the fact that emerging and developing economies are likely to fare worse than advanced economies, despite GDP projections suggesting that the magnitude of the 2020 recession was less acute for low-and middle-income countries (Figure 1). This can be illustrated by computing GDP losses relative to the pre-COVID era (2019) across regions of the world (Figure 2). With the exception of China, in all cases, regions that form part of emerging and developing economies are expected to experience higher GDP losses relative to advanced economies.

Source: Derived from IMF, World Economic Outlook, January 2021

Notes: Em. Asia ex.CHN= Emerging Asia excluding China; LAC= Latin America and the Caribbean; MECA= Middle East and Central Asia (MECA); Em.Eur = Emerging Europe; AE= Advanced economies

Labour market indicators suggest that lower middle-income economies are expected to experience a greater degree of labour market distress relative to their counterparts in both rich and poor countries. The latest (January 2021) ILO estimates indicate that work-place closures have led to a loss of 8.8 percent of workhours globally relative to 2019 thresholds in 2020. This is distributed as follows: low-income countries – 6.7 percent; lower middle-income economies- 11.3 percent; upper middle-income countries: 7.3 percent; high income countries – 8.3 percent. Similarly, the share of labour income losses due to workhour losses are of greater magnitude in lower middle-income countries relative to their counterparts in low, upper middle-income and high-income countries.

If one adds the impact on extreme poverty of COVID-19, then the picture of the greater distress experienced by low- and middle-income economies becomes even more stark. Given the way that extreme poverty is currently measured (the ‘global’ poor earn less than USD 1.90 a day), it is almost exclusively prevalent in low- and middle-income economies. Until COVID-19, extreme poverty was on a sustained downward trend. Now, the latest estimates suggest that “… between 119 and 124 additional poor globally ” as a result of the pandemic (Lakner et al, 2021). What is worrying is the steady manner in which the pertinent projections have worsened. In April 2020, for example, the maximum expected increase in global poverty was 62 million. By January 2021, this has more than doubled.[4] Some of the most populous countries in South Asia, such as India, are projected to experience the highest increase in poverty (Kharas, 2020). In contrast, in some advanced economies, such as the USA, a generous, but time-bound, increase in income support was associated with stability in short-run poverty during the early phase of the pandemic.

One area that has been badly hit is the education of children and young adults. In April, when the first wave of COVID-19 was at its peak, more than 90 percent of children were subjected to school closures globally. At the same time, various tertiary institutions, most notably technical and vocational institutions, were badly affected. While the situation has eased to some extent, the deleterious long-term consequences are increasingly becoming evident. World Bank estimates note that ‘learning poverty’ (inability to read a simple text by age 10) is projected to increase from 53 percent of the pertinent cohort to 63 percent in low and middle-income economies. This in turn translates into potential earning losses almost equal to 10 percent of the collective GDP of middle-income economies.

In sum, the challenges that low and middle-income economies will face in a post-COVID world are immense. It will require a combination of national determination and generous international cooperation to attenuate these challenges.

………………………………………

[1] See, for example, Jones (2020) and Bheemaiah et al (2020)

[3] Economic Tracker (tracktherecovery.org). The data is based on November 15, 2020

[4] Lakner et al, 2021

Just wondering … Are you from Gujarat too? If so

LikeLike