In an iconoclastic paper, Lant Pritchett and Larry Summers (2015), question the standard view that emerging economies in the Asian region that are currently growing rapidly are expected to do so for the next decade and beyond. The authors call this a case of ‘Asiaphoria’. Yet, they argue, an enduring feature of growth statistics is that there is ‘regression to the mean’, that is, over time even rapidly growing economies converge to mean rates that lie between two and four percent. Hence, ‘abnormally rapid growth’ does not last too long. As countries grow richer, their growth rates slow down. One can also call this a case of secular growth slow-down. Summers and Pritchett argue that the most popular case of Asiaphoria is represented by China. Yet, China is not immune to the phenomenon of a secular growth slow-down – see Figure 1 below.

Figure 1

Source: Pritchett and Summers (2015)

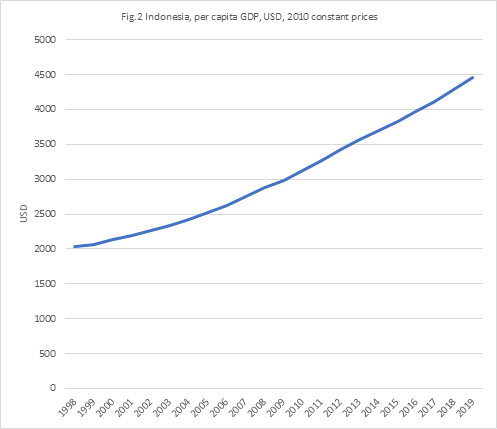

What about other Asian economies, such as Indonesia? It had the misfortune of suffering from a historically unprecedented double-digit recession in the wake of the 1997-1998 Asian Financial Crisis. This was followed by decades of solid growth of just over 5 percent.

Despite such impressive achievements , there is a yearning among policymakers to grow at an even faster rate that is at par with the rapid growth era of the Suharto regime when, between 1980-1996, the economy grew at an average rate of seven percent. This aspiration is one of the reasons behind the current push for comprehensive structural and regulatory reforms. The expectation is that such reforms will allow the replication of the golden period of growth of the 1980s and mid-1990s – or at least a growth rate in the six percent range.

Figures 2 and 3 depict the average long run growth rate of Indonesia (5.5 percent) – measured over four decades – relative to seven selected economies from ASEAN and OECD and adds a new metric: the number of recessions per country over forty years. Indonesia’s long-run growth performance is commendable relative to regional and OECD norms. It is noteworthy that Indonesia had fewer recessions (two) than the selected OECD economies (five to seven) and some ASEAN economies (three).

Derived from IMF DataMapper

Derived from IMF DataMapper

The key issue is whether it is reasonable to expect that Indonesia should aspire to grow at even faster rates – six percent seems to be one of the aspirations – for the next decade and beyond.

Will Indonesia succumb to a secular growth slow-down? If so, does it matter? Figure 4, derived from long-run projections by the OECD (2018), suggest that aggregate growth rate will decline by one percentage point between now and 2030 – thus corroborating the notion of a (partial) regression to the mean.

Source: Derived from OECD (2018)

Optimists suggest that it is possible to avoid the phenomenon of secular growth slow-down by adopting an ambitious agenda of structural and regulatory reforms cutting across governance and education. In the case of Indonesia, such reforms are projected to increase the aggregate growth to a moderate degree – but not to the six percent threshold. It is, however, reassuring to note that, even in the case of a ‘business-as-usual’ scenario, Indonesia’s per capita GDP is expected to increase from 30.5 percent of OECD-wide per capita GDP to 48 percent by 2045 . At that point, Indonesia will be celebrating its 100th year as a sovereign nation.

This terse, but important, discourse on secular growth slow-down implies that one should avoid the temptation to succumb to ‘Asiaphoria’. The emphasis should be on the quality of growth rather than its quantity. This, in turn, entails an understanding of the employment and social dividends that accrue at a given rate of growth and how to enhance such dividends with an appropriate mix of policies.