Offers succinct commentary on topical issues that cut across both rich and poor countries. Entails critical insights on poverty, inequality, health, macro-policies and many more

Mortality statistics have a direct bearing on life expectancy (at birth). Higher morality leads to lower life expectancy and vice versa. COVID-19 represented a major mortality shock over the last 70 years, but its impact was uneven across the world.

The United States experienced the third highest loss in life expectancy because of COVID-19 in a sample of 29 high income countries. Only Bulgaria and Slovakia had worse outcomes. It is also worth noting that: ‘in the United States, the pandemic has accentuated the pre-existing mid-life mortality crisis’. (Scholey, 2022).

The countries that do well are in Northwest Europe, especially the Nordic countries.

Paul Krugman suggests that the decline in life expectancy in the United States is regionally concentrated with ‘red states’, where political conservatism holds sway, suffering disproportionately from COVID 19 deaths.

There is a statistically significant negative association between the magnitude of the decline in life expectancy and vaccination uptakes – high declines are associated lower vaccination incidence.

Figure 1: COVID-19 and life expectancy in a sample of high income countries

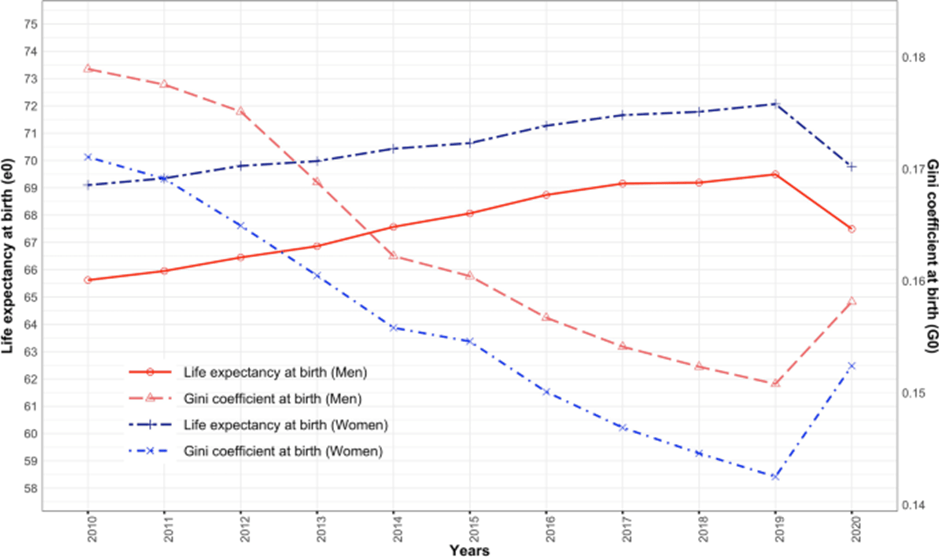

Here is a chart which looks at both life expectancy at birth for men and women (eO) and inequality in life expectancy as measured by the Gini coefficient (gO) over the 2010-2020 period in India. There is a sharp decline in life expectancy among both men and women between 2019 and 2020, with levels equivalent to what prevailed in 2010 for women and 2014 for men. In terms of years lost, ‘…the mortality pattern of COVID-19 reveals a drop of 2.0 and 2.3 years for men and women, respectively, between the pandemic year 2020 and the non-pandemic year 2019’. (Yadav et al, 2021).

Inequality in life expectancy – which was falling consistently between 2010 and 2019 rose sharply after that. In sum:

“The COVID-19 pandemic has negative repercussions on life expectancy and inequality in age at death and has slowed the mortality transition in India.”(Yadav et al, 2021)

I reflect on how and why Gautam Adani – a leading member of India’s Billionaire Raj – became the victim of a stock marker rout. He was once regarded as the second richest man in the world. His net worth has taken such a hit that he is now ranked the 18th richest in the world, while his group of companies has lost more than USD 100 billion within the space of a week.

Rishi Sunak’s spectacular rise in British politics has understandably drawn a great deal of global attention. His achievements are indeed for the history books: the first ever non-white British Prime Minister of Indian heritage who is also a practicing Hindu; the youngest in more than 200 years. His conspicuous status as one of the richest Prime Ministers in British history owes much to his marriage to Ms Akshata Murthy, the daughter of the Indian tech billionaire Narayana Murthy. Rishi Sunak, like very many British former Prime Ministers, is the beneficiary of elite education (Winchester College, Oxford, Stanford Business School).

In September, it appeared that Rishi Sunak was destined to become the ‘nearly man’ having lost comprehensively to Liz Truss when the rank-and-file members of the Conservative party voted for her in droves. There was a certain irony in the ascension of Liz Truss because Rishi Sunak was blessed with a strong show of support by his fellow MPs but the plebians in the party decided to disregard the collective will of the plutocrats in Parliament.

Fate smiled on Rishi Sunak when the Prime Ministership of Liz Truss imploded spectacularly in the wake of her pristine neoliberal agenda of using unfunded tax cuts, primarily directed towards the rich, to drive growth. The ‘markets’ rebelled at such fiscal profligacy at a time of high inflation and rising public indebtedness spelling the end of Ms Truss and her Prime Ministership. She could only depart with the indelible label of the shortest serving Prime Minister in British history. This paved the way for Rishi Sunak’s rise facilitated by the ‘kingmakers’ of the Conservative Party (the 1922 Committee) who changed the rules of selection to give a very high degree of weight to a candidate’s popularity among MPs. The only remaining contender (Penny Mordaunt) did not stand a chance, while the disgraced former Prime Minister Boris Johnson, seeking a triumphant return, simply gave up. Rishi Sunak was duly anointed as the leader of the Conservative Party without even having to seek endorsement from rank-and-file members.

Does the rise of Rishi Sunak in British politics herald a new era for ethnic minorities in multicultural Britain? As someone who lived in the UK for ten years during the early 1970s and early 1980s as a student (A levels and University education), I was struck by how far Britain of that period has evolved. I still recall the racist slurs (‘Paki’) that were occasionally directed at me and my family and the horrendous bashing from racist thugs that two of my friends endured. As Aamna Mohdin notes, ethnic minorities at the time were subjected to a ‘sustained campaign of terror’ by nativist agitators. Furthermore, in 1980, the year Rishi Sunak was born, there was not a single person of colour in the British Parliament. Multicultural Britain of the 21st century has thankfully moved beyond the primitive rage of the nativists of the 1970s and 1980s.

Image 2: ‘Skinheads’ in the 1980s notorious for being associated with ‘Paki-bashing’.

It is thus legitimate to ask: does the phenomenal political elevation of Rishi Sunak mean, as Indian politician Shashi Tharoor who is also a fierce critic of British colonial rule says, that Britain has ‘outgrown racism’. I am not so sure. I like to think that the British Conservative Party consists of overt racists and forward-looking realists prepared to allow for pragmatic accommodation with ethnic minorities. Racists are captive to primordial emotions that overcome their judgements. Hence, they yearn for an insular and nativist agenda that belies current circumstances. Realists know how to hide their racial prejudices while having full faith in the superiority of Western/European civilisation. Realists know that the UK, for decades now, has embarked on an irreversible path towards a multicultural, multi-faith future. Realists realise that there are many potential Rishis in waiting. They can no longer be ignored as natives who serve ‘vindaloos’ to white clients or mind the corner store through all sorts of odd hours. Furthermore, realists feel much more at home with the ‘pucca sahibs and begums’ of colour rather than the ‘white trash’ in some forgotten part of Northern England who can’t even speak English with the right accent. More importantly, the realists are fully aware that these pucca brown sahibs and begums can be relied upon to project a ‘holier-than-thou’ attitude to demonstrate their Britishness. Hence, one has the glaring example of Suella Braverman who has returned as home secretary to continue her role as aggressive culture warrior and who is keen to pursue her anti-immigration agenda. She is also on record as saying that Britain should not feel apologetic about its colonial past. In sum, I would argue that the realists in the Conservative Party are happy to have the fig leaf of diversity reflected in Rishi Sunak and many of his colleagues who are in the frontbench.

Video insert of Suella Braverman extolling the virtues of the British Empire

There are multiple reasons to believe that Rishi Sunak is most unlikely to disrupt the status quo of an iniquitous society that cuts across class and race. Hence, the Conservative Party is in a safe pair of hands. His coronation does not connote a new era for multicultural Britain. Rishi Sunak is a self-proclaimed ‘proud Thatcherite’. He voted for Brexit. He believes in a low tax, fiscally conservative regime. He will be preoccupied with soothing the frayed nerves of the markets through fiscal consolidation regardless of its socio-economic consequences. This is a conventional Conservative way of responding to economic challenges. Hence, one might see a replay of the fiscal austerity program under David Cameron that ‘broke Britain’.

Broken Britain today manifests itself in many ways, but most notably in large-scale poverty and deprivation. According to the comprehensive poverty line devised by the Social Metrics Commission, 22 percent of the population were deemed to be poor even before COVID-19. Ethnic minorities were conspicuous for very high poverty rates. Other surveys show that nearly 5 percent of the population are ‘food insecure’ with a sustained increase in the utilisation of foodbanks. With an incipient energy crisis and the lingering effects of COVID-19, poverty in the UK is likely to get worse. Do not expect Rishi Sunak to acknowledge these challenges and seek to act upon them. It is only a matter of time before the first person of colour to become British Prime Minister shows his true ideological colours.

There are, as Ronald Suny points out, two contending narratives on the brutal Russian invasion of Ukraine and the humanitarian catastrophe that it has created. The dominant version familiar to many in the West is that Ukraine is the hapless victim, and perhaps the first of many, of Russian neo-imperialism. The architect of neo-imperial intent is Vladimir Putin. Such a narrative is enunciated as a morality play, with a cast of characters that range across victims, villains, and heroes. It is a story in which the victim, a morally righteous David (in the form of President Zelensky of Ukraine), is pitted against a vile and villainous Goliath (manifested in the Russian President Putin). US-led Western heroes of NATO are aiding and abetting David with weaponry, financial assistance, moral support, UN-led condemnations, and crippling sanctions on Russia. They are protecting liberal democracy in Ukraine in particular and East Europe in general. They are defending a ‘rules-based’ global order.

At the same time, the US and its Western allies are exercising restraint because they are ruling out any attempt to engage in a direct confrontation with a nuclear-armed Russia. The expectation is that this strategy will pay off as Russia concedes defeat and decides to end its invasion of Ukraine. Any attempt to seek a negotiated settlement with Russia is seen as appeasement which will only embolden Putin. It will entail a betrayal of the aspirations of the Ukrainian people to remain a sovereign nation and embrace the liberal democratic West through eventual EU and NATO membership.

The alternative view is that the perfidious Russian invasion of Ukraine is a tragedy foretold, especially by foreign policy experts and scholars of international relations in the US. Its roots lie in egregious errors of US foreign policy, and it has to do with NATO.

It was under President Bill Clinton that the project to expand NATO ‘eastward’, that is, to incorporate the ex-Soviet Republics in Eastern Europe, gathered pace. Bill Clinton and his cheerleaders celebrated such expansion. Then-Senator Joe Biden played a pivotal role in this cheerleading exercise proclaiming that ’50 years of peace’ was within the grasp of humanity. Much more knowledgeable observers were alarmed.

On June 26, 1997, a group of 50 prominent US foreign policy experts that ‘..included former senators, retired military officers, diplomats, and academicians, sent an open letter to President Clinton outlining their opposition to NATO expansion’. They considered a ‘…US-led effort to expand NATO (to the former Soviet Republics) ‘ as a ‘…policy error of historic proportions’. They highlighted the fact that ‘In Russia, NATO expansion…continues to be opposed across the entire political spectrum’ which will ‘…bring the Russians to question the entire post-Cold War settlement’. They proceeded to argue that Russia, struggling to recover from the political and economic calamity of the dissolution of the Soviet Union, ‘…does not now pose a threat to its western neighbours and the nations of Central and Eastern Europe are not in danger’. This warning was duly ignored and the US Senate ratified NATO expansion starting with Poland, Hungary, and the Czech Republic in April 1998.

‘I think it is the beginning of a new cold war. I think the Russians will gradually react quite adversely and it will affect their policies. I think it is a tragic mistake. There was no reason for this whatsoever. No one was threatening anybody else. This expansion would make the Founding Fathers of this country turn over in their graves. We have signed up to protect a whole series of countries, even though we have neither the resources nor the intention to do so in any serious way. [NATO expansion] was simply a light-hearted action by a Senate that has no real interest in foreign affairs.’

In 2007, Vladimir Putin gave a much-noted speech at the Munich Security Conference (MSC) where he expressed his clear disapproval of a US-led ‘unipolar model’ that emerged after the end of the Cold War proclaiming that ‘I consider that the unipolar model is not only unacceptable but also impossible in today’s world’. Most importantly, he observed:

‘NATO expansion … represents a serious provocation that reduces the level of mutual trust. And we have the right to ask: against whom is this expansion intended? And what happened to the assurances our western partners made after the dissolution of the Warsaw Pact? Where are those declarations today?’

Yet, in April 2008, the US and its NATO allies welcomed Georgia and Ukraine to be members of NATO, although when it was likely to happen remained unspecified. The irony is that, as Stephen Walt points out, Ukraine was a non-aligned country until then.

One could argue that Russia’s response to the ‘serious provocation’ (Putin’s words as uttered in 2007 – see above) of NATO expansion entailed the use of military force and the use of pro-Russian proxies to protect its security concerns. The Russo-Georgian war of 2008 is consistent with this interpretation. The annexation of Crimea in 2014 and a grinding conflict in Eastern Ukraine led by pro-Russian separatists might be seen as responses to the so-called Maidan revolution that led to the ouster of a pro-Russian Ukrainian President. Sadly, in this contentious affair, the US was not an innocent bystander. As Ted Galen Carpenter notes, US politicians openly aided and abetted the progenitors of the Maidan revolution in which unsavoury far-right political forces played an important role.

Those who support the view that NATO’s reckless eastward expansion and its offer to incorporate Ukraine as a member of NATO at some point in the future provoked Russian aggression also point out that the US would react in much the same way if faced with similar circumstances. Suppose Mexico was to seek a security alliance with Russia or China and allowed its territory to host foreign army bases. The US would react aggressively. This, Peter Beinart explains, would be a re-affirmation of the Monroe Doctrine formulated nearly 200 years ago in which the US states that it has the unique right to exercise its sphere of influence in its own hemisphere and any attempt by ‘foreign powers’ to tamper with this right will be perceived as ‘dangerous to its peace and security’. Hence, Putin’s 2007 proclamations appear to be a Russian version of the Monroe doctrine.

It is impossible to prove the veracity of this interpretation of the historical context to the current tragedy that is unfolding in Ukraine today. It is entirely possible that Russia would have invaded Ukraine even in the absence of NATO enlargement. This counterfactual cannot be dismissed, but those who subscribe to it do not have a tangible solution other than seeking the comprehensive defeat of Putin’s Russia. Short of this seemingly unattainable goal, what is a way forward?

Sanctions are certainly likely to cripple the Russian economy, while indirect military support to Ukraine would sustain this highly uneven conflict between David and Goliath. Despite sanctions, Russia will probably continue its brutal military interventions in Ukraine simply because sanctions, while causing a great deal of pain borne by ordinary people, do not lead to changes in the core strategy of a particular regime (think of Cuba, North Korea, Iran, Venezuela and similar examples). As the IMF has warned, the longer the crisis in Ukraine persists, the greater the adverse consequences on the global economy. This is primarily because of adverse energy and food price shocks caused by further disruptions to supply chains already reeling under the impact of COVID-19. The poor and vulnerable in parts of the world far removed from Ukraine are likely to bear the brunt of adverse price shocks.

Those who subscribe to the view that NATO’s eastward expansion is a central part of the narrative on the war in Ukraine suggest it ‘could really be ended with a diplomatic solution in which Russia withdraws its forces in exchange for Ukraine’s neutrality’ (Jeffrey Sachs). There are small, prosperous countries in Europe, such as Finland, that peacefully co-exist with Russia without being members of NATO. Henry Kissinger, perhaps the personification of the US foreign policy establishment and leading scholars of international relations – such as Stephen Walt,John Mearsheimer, and others – fully concur with this prescription of ‘Finlandization’ of Ukraine.

Micheal Mandelbaum, one of the 50 who raised formal objections to the NATO enlargement project in 1997, has wistfully reflected on an alternative scenario. ‘Imagine, he says, a different global configuration, with Russia aligned with rather than opposed to the United States’. Indeed. Imagine!

Durable global and regional peace is likely to happen when the US and its Western allies move away from treating Ukraine as a morality play in which they, and they alone, are the defenders of a rules-based international order in a multi-polar world. Will they have the humility to acknowledge that the NATO enlargement project has probably led to unintended, but tragic, consequences? Will they embark on the delicate task of persuading the current regime in Ukraine that its best future lies in being a non-aligned nation buttressed by mutual security guarantees from Russia and the US and its allies? Will the West, in cooperation with Russia, be prepared to offer a massive reconstruction package to enable Ukraine to move beyond the ruins of war? Only time will tell.

The Royal Commission Report into Misconduct in the Banking, Superannuation and Financial Services Industry will be released to the public this afternoon (4 February 2019). The Commission had already published an Interim Report in September 2018.

The Interim Report had hardly anything good to say about the industry. Rather, the Commission used the word “greed” to describe the industry’s behaviour and how the industry largely treated the ordinary customers. Otherwise, how can one explain fees charged for services not provided? Fees charged to dead people?

The Australian banking industry had been politically very successful for decades. In the post-GFC years, the industry used the excuse of ‘rising costs of funds’ in international markets for raising their interest rates asynchronous to the RBA’s rate decisions. Nobody raised an eyebrow when the major four banks reported record profits year after year while still crying poor about rising costs of funds. The crux of the matter is the banking industry fell into a culture of profit at any cost and bank executives’ remunerations were linked to profit and revenue. Thus, the bank executives in Australia all they cared for was whether they were contributing to the bank’s revenue and profit. Bank leaders did not care enough whether their employees were doing the right thing for their customers. If the bank management were thinking that they were more focused on creating shareholder wealth, shareholders thought differently. ANZ, NAB, and Westpac – all received a ‘first strike’ 2018 under Australia’s ‘two strikes’ rule. CBA received a ‘first strike’ in 2016.

So, the bottom line is: yes, we want our banks to be profitable and financially strong. Yes, we need strong banks for a strong economy. But the profit must be clean.

Bangladesh has endured political upheaval before. What made the recent interim period stand out was not protest or dissent, but the scale and normalisation of mob violence—vigilante attacks, public beatings, and political reprisals carried out openly. According to the European Agency for Asylum, Bangladeshi human rights organisations “…documented the highest rates of deaths due to mob beatings in a decade”. This did not happen because Bangladesh suddenly became more violent. It happened because, at a critical moment, authority hesitated. That authority was led by Professor Yunus, a Nobel laureate.

Interim governments exist for one primary reason: to stabilise the state during transition. They are not ceremonial caretakers. They govern during the most fragile phase of political life, when early decisions shape long‑term outcomes. In Bangladesh, that responsibility was not met.

Authority existed — and that is the point

The most important fact in this debate is often overlooked: the Bangladeshi state did not collapse during the interim period. Police forces remained in place. Courts functioned. The administration operated. International recognition was strong. Authority existed.

Political philosopher Hannah Arendt makes a distinction that is crucial here. Power, Arendt argues, rests on legitimacy and collective acceptance. Violence appears when that power is weakened or abdicated. When violence spreads, it is usually not a sign of popular empowerment, but of authority failing to act.

Seen this way, Bangladesh’s experience points to omission rather than inevitability. Leaders do not need to encourage violence to be responsible for its spread. Hesitation, delayed enforcement, and mixed signals are enough. In fragile institutional settings, restraint is rarely read as wisdom. It is read as permission.

How perpetrators of mob violence learned they enjoyed impunity

Sociologist Charles Tilly helps explain how this dynamic unfolds. He shows that mob violence is shaped by signals and incentives, not chaos. People watch what happens after the first incident. If early violence is punished quickly and consistently, it often subsides. If it is not, others follow.

Bangladesh fits this pattern. Analysts inside the country have pointed out that mob violence did not previously occur at this scale. Its expansion followed a familiar sequence: early incidents went insufficiently addressed, expectations of impunity formed, imitation followed, and violence became normalised. Each unpunished act lowered the threshold for the next.

Once this process begins, restoring order becomes far more difficult. By the time condemnations are issued, the street has already learned that enforcement is uncertain.

This was not inevitable

Defenders of the interim period often argue that the violence was unavoidable given the intensity of political change. That argument is weak. Transitions are volatile everywhere, but they also offer a narrow window where clear boundaries can be set. Early arrests, visible prosecutions, and unambiguous messaging can quickly shape behaviour. Bangladesh missed that window.

This is not a cultural story, and it is not about importing ideas from abroad. Modern democracies do not practise vigilantism. The issue is contextual misjudgement—applying restraint suited to strong institutional environments in a weak one.

The lesson and an anti-thesis of Arendt and Tilly

Bangladesh’s experience offers a stark lesson. Interim governments wield real power, even if temporarily. When that power is not exercised clearly and early, violence fills the gap. Arendt explains why violence signals failed authority. Tilly explains how inaction turns disorder into routine. Together, they show why mob violence in Bangladesh was not fate, but the result of a missed moment—and why accountability for that failure matters.

The above would partially explain according to Arendt and Tilly. The real reason is the disposition of the central character of the mob violence, Professor Yunus. It may sound preposterous but reflecting on his rule, or rather misrule, one can easily argue, that he came with a personal vendetta against the previous Government. He seized the opportunity to expand his own agenda of the Grameen group taking over many sectors. The mob violence was a “false flag” for him!

The American author William Irving created a famous fictional character called Rip Van Winkle who drinks a magic potion and wakes up decades later to find that his personal world and the world around him have changed greatly. Winkle observes both positive and negative changes.

Imagine that the magical properties of Rip Van Winkle are embodied in an 18-year-old Rahim. He is a staunch Bengali nationalist. Rahim is a witness to epochal events: the Bangladesh War of Liberation that started on 26 March 1971 and ended on 16 December 1971; the emergence of Bangladesh as a new nation; the devastating famine in 1974 in which more than a million people perished; a highly contentious political experiment of a one party state that lasted between January and August 1975; the gruesome assassination of Sheikh Mujib and most members of his family in mid-August 1975, the founding father of the nation and its first elected Prime Minister; the trauma and turmoil that followed.

In a state of despair and desperation that his expectations of a peaceful and prosperous Sonar Bangla (Golden Bengal) were dashed, Rahim drinks a magic potion and falls into a long and deep slumber. He wakes up in contemporary Bangladesh. He is now an old man well past 70. What does he see? What will he say?

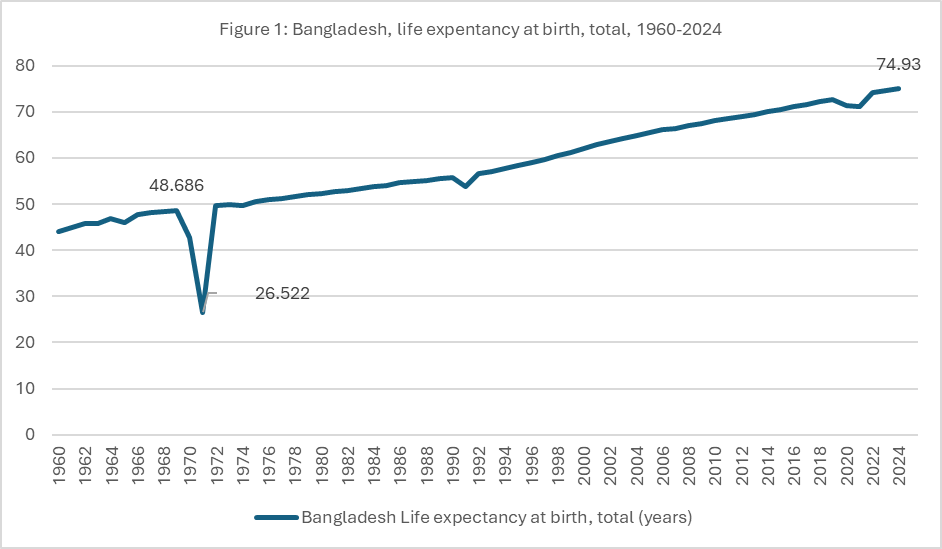

As a staunch Bengali nationalist, he would certainly be elated at the economic progress that has taken place. The average Bangladeshi today can expect to live around 75 years. It is difficult to imagine that life expectancy in Bangladesh in 1971 plummeted to 27 years (!) during the War of Liberation before recovering to 49 years in 1972 – see Figure 1.

Rahim would also note that such statistics is a powerful vindication of the view that huge losses of life and displacement of people took place during the War of Liberation and one that was primarily caused by genocidal acts of the Pakistan army and its local collaborators. He would lament the fact that those who committed such war crimes were not held accountable for such gruesome acts. The Pakistani soldiers and army officers who occupied Bangladesh as perpetrators of violence against innocent civilians between March and December 1971 were given a safe return to Pakistan (thanks to the magnanimous gesture of the Indian government of the time). Some local collaborators were tried, found guilty and given the death penalty, but most escaped any form of accountability. Rahim must wonder: when will this culture of immunity end?

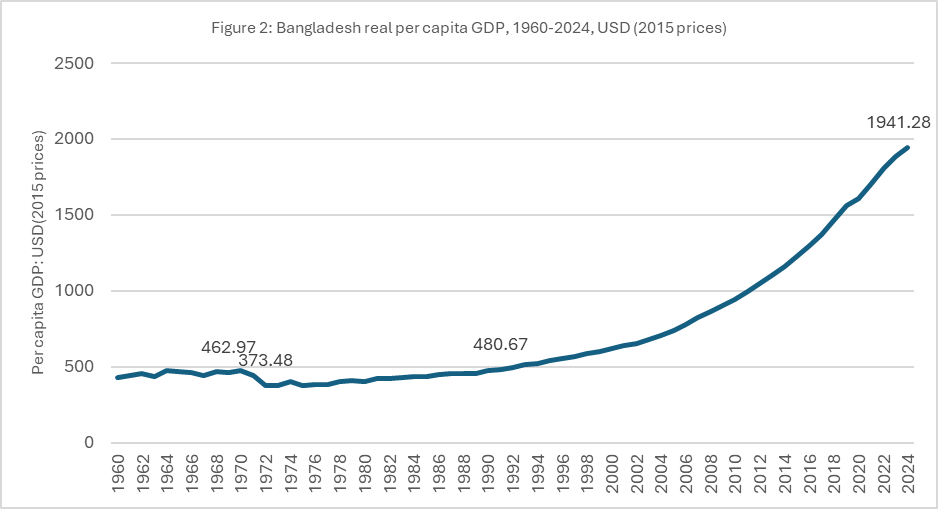

If one uses another basic metric of living standards, per capita real GDP, Rahim would simply be stunned at the scale of the progress that has taken place. Between 1969 and 1972 per capita real GDP contracted by 19 per cent. Today, per capita GDP is 5.2 times the level that prevailed in 1972 – see Figure 2. Furthermore, as a recent World Bank assessment (October 2025) notes:[2]

Between 2010 and 2022, real GDP grew by 6.6 percent annually, nearly doubling GDP per capita and reducing poverty at the extreme national poverty line (lower) from 12.2 to 5.6 percent and at the absolute national poverty line (upper) from 37.1 to 18.7 percent. Multidimensional poverty also declined from 46.8 to 21.3 percent, alongside improvements in health, education, sanitation, and electricity access.

Rahim can barely reconcile these numbers with the Bangladesh that he witnessed in 1971-72 and during the famine of 1974. Poverty was endemic. He would heartily endorse the view that “Bangladesh has lot to be proud of”.[3] He can say that he comes from an era in which Bangladesh was denigrated as a “basket case” and there was extraordinarily little to be proud of. This, he would proclaim with a deep sense of satisfaction, is a vindication of all the optimists – most notably Mujib and his generation of nationalist politicians and fellow travellers – who fervently believed in the idea of Bangladesh long before it became a reality. Indeed, he would go even further and say that Bangladesh would, today, be worse off had it remained as a province of Pakistan. In core areas of well-being, Bangladesh as an independent nation has outperformed Pakistan. For example, life expectancy in Bangladesh is about ten years more than Pakistan, while its literacy rate is twenty percentage points higher than Pakistan’s.[4]

Yet, like Rip Van Winkle, Rahim must highlight adverse changes. To start with, he would find the capital city Dhaka clogged with traffic and bursting at the seams with high rise apartments and buildings. The air quality in Dhaka is among the worst in the world.[5] He is alarmed at a report that about 30 percent of the population face heightened climate risk. The Dhaka that he left in the 1970s was much poorer but quieter and cleaner. Global warming and its deleterious consequences were not part of the policy agenda.

Rahim would be aghast at the grotesque levels of inequality and the endemic corruption that pervades everyday life. One study, based on a ‘corruption perception index’ (CPI), finds that “the global average score out of 100 (which is best) is 42, while Bangladesh’s score is 24—which is 18 points lower than the global average score and 21 points lower than the Asia Pacific region’s average score of 45”.[6] Furthermore, the same study finds that Bangladesh’s ranking since 2023 has not changed, despite major political transitions.

Despite notable socio-economic progress, Rahim would note that new challenges have emerged. The latest reports suggest that in the post-2022 period, both overall and extreme poverty have increased in Bangladesh.[7] Growth has slowed down, while the global political and economic climate, following the war on Iran, has worsened. Bangladesh, like many countries in the world, faces a fuel crisis which is being driven by external factors.

It is on the political front that Rahim has the most concerns. He was shocked to realize that Sheikh Hasina, who was reportedly a timorous, soft-spoken housewife, turned out to be a ruthless politician who became the longest serving female Prime Minister in the country’s history. At the same time, her attempt to hold on to political power by force made her vulnerable. She was ousted in a violent uprising in August 2024 and was forced into exile. There is a judicial ruling against her that entails the death sentence for committing crimes against humanity. Rahim would be deeply saddened to note how Hasina, in a bid to deify her father’s memory, ended up destroying his legacy. The Awami league that Rahim knew is now in the political wilderness from which it might never return.

Rahim is left wondering how the new Bangladesh will evolve. The key power brokers, now led by the Bangladesh Nationalist Party (BNP), as well as the official Opposition, led by Jamaat, represent a constellation of forces that are keen to construct a durable historical narrative that will be inhospitable to the values and principles that animated a generation who fought selflessly for the idea of Bangladeshi nationhood. In that fundamental sense, Rahim wonders whether Bangladesh has really progressed beyond the 1970s. A political culture of immunity, violence and vendetta that were so evident in the mid-seventies remain ever-present dangers.

Viral Empire: How Microbes Reflect Human Power Structures

By Aunul Islam, PhD (Imperial College, UK)

Modern power no longer operates primarily through borders or armies but through networks—supply chains, information flows, technology, and interdependence. In this sense, contemporary geopolitics resembles microbial systems more than traditional empires.

Microbes exert influence through connectivity, adaptation, and asymmetry. Small organisms can destabilise large systems by exploiting vulnerabilities, just as minor interventions can trigger outsized effects in a networked world. Power depends less on scale than on speed, positioning, and resilience.

Like microbes, political systems evolve under pressure. Expansion produces resistance, cooperation strengthens survival, and rigid structures fail in volatile environments. The greatest risk is not defeat by rivals but internal systemic collapse.

Seen this way, global power functions as a living ecosystem—adaptive, fragile, and continuously contested rather than permanently controlled.

In the above narration, the scientific expressions like mutation, virulence in the microbes behaviour have been translated in the business and strategic literature to relate them to humans. But this literature lacks sufficient emphasis on the destruction through wars and conflicts by humans on core aspects of their own life. This entails destruction of properties and other supporting elements such as hospitals, energy production etc.

At this juncture, the anti-thesis to above narratives is that human empire or a Supreme Empire do not adhere to the simple modalities in present day geopolitics. The present empire dictated by a lone country (USA) along with its lackeys is no longer a traditional empire as depicted previously. The viral empire like that of the bubonic plague or even the Covid-19 virus are now long forgotten past. The present Super Empire is best described as the worst of its kind, genocidal in nature and any other terms that can be used to describe it, where new words have to be added to the dictionary.

The last hope of the present world order is that the super empire does behave like a viral empire and succumbs to its own systemic collapse. Maybe this will happen in the next few decades!

There are several reasons why one can be optimistic about the survival of the current regime in Iran following the illegal and unprovoked war on the nation waged by the USA and Israel. First, the regime managed to overcome its most dangerous and fragile moment, that is, immediately after the assassination by Israeli bombs of Khamenei, his family members and his entourage of senior leaders. At 86, and after having ruled Iran for 40 years with an iron fist, Khamenei decided to become a martyr. Hence, he was at his office – a publicly disclosed location – when he was killed. This was both a spiritual and strategic move. Martyrdom plays a vital role among the Shia faithful. The decision to die in this manner was strategic because it signalled to the Iranian population that a succession plan was in place in line with constitutional provisions. Iran is a constitutional republic that has endured for 50 years. It is not a lawless theocracy dependent on the whims of an aging Ayatollah.

Second, and this follows from the first, Trump and Netanyahu failed to understand the multi-layered structure of the Iranian regime. They thought with Khamenei and his senior entourage gone, the regime would collapse and the thankful Iranians would dance with joy in the streets and enthusiastically engage with a new pro-American and pro-Israeli political settlement. Both Trump and Netanyahu would declare victory and go home. This did not happen. Instead, the regime maintained its constitutional continuity. The bombing continues, hundreds have been killed so far (550 at last count). It is difficult at this stage for the average Iranian to treat the Americans and Israelis as liberators when they are being killed and maimed by made in USA bombs and missiles.

Third, Iran has shown that it can retaliate against the combined military might of USA and Israel by using a most potent weapon of modern warfare – long-range (but not intercontinental) ballistic missiles that draw on North Korean, Russian and Chinese expertise. According to some estimates, Iran possesses more than 3,000 of them. Admittedly, both USA and Israel have so-called interceptors, that is, defensive technology that can intercept incoming missiles. But, as Israel is finding to its cost, such a technology is not fool-proof. Most importantly, the very sophistication of this technology is also its Achilles Heel. It is extremely expensive to operate, stocks are limited and has high turnaround times to replenish. It has been suggested that neither the USA nor Israel has the capacity to sustain full-scale use of the interceptors beyond a few weeks before critical shortages emerge.

Fourth, Iran has fully adopted the tools of asymmetric warfare which weaker parties deploy against formidable adversaries. Unlike the last war (June 2025), when it was attacked by Israel, Iran decided from the very beginning that there are no ‘red lines.’ Hence, it is hitting the Arab allies of USA in the Gulf monarchies and causing them considerable grief and consternation. This is being done by inflicting damage on US bases hosted by the Gulf states, targeting sensitive civilian assets entailing airports, ports, luxury hotels and energy infrastructure. The result is mayhem. The famous airlines of the Middle East – Emirates, Etihad and Qatar – are all grounded. ‘Hundreds of thousands of travellers’ are caught in limbo. The carefully curated images of Bahrain, Dubai, Abu Dhabi and Doha as safe playgrounds for affluent, hedonistic hustlers have been severely damaged. Most importantly, energy prices are projected to rise sharply, partly because countries such as Qatar have temporarily stopped LNG production. Iran has also choked off traffic in the Straits of Hormuz to a trickle. This is highly significant because Hormuz hosts oil tankers that supply 20-30% of the world’s oil.

The attack on the Arab allies of USA might appear that an Iranian regime is lashing out against its neighbours in desperation, but the strategic rationale is different. By attacking the Gulf states in such a brazen way, Iran is sending a clear message: US protection of its Arab allies means extraordinarily little when push comes to shove. This is a move by the Iranians that was not part of the strategic calculus of USA and its allies.

Fourth, it is by no means clear that Trump has the appetite for a long war which is deeply unpopular among Americans (75% oppose the war on Iran, according to some polls). He has brazenly broken his election pledge that there will be no more ‘wars of choice.’ Trump’s approval rating is low. His MAGA base is becoming restless, caught in the grip of a cost-of-living crisis that is likely to worsen with the projected increase in energy prices. Mid-term elections are approaching and Trump has little to show as accomplishments other than vacuous showmanship. American military personnel are paying for Trump’s war of choice with their lives – six dead so far with many more injuries. The pain threshold for the average American is low when such needless deaths occur.

In sum, ‘victory’ for Iran means regime survival even when facing formidable foes. If Iran can pull it off, it will be seen as the mythical David prevailing over Goliath. Of course, the costs will be extremely high in terms of death and destruction and adverse economic consequences that will linger for years, but the Iranian leadership could say that it did not choose this suicidal path. It was forced to defend the nation against implacable and powerful enemies.

Note that Trump left the Maduro regime intact, with the Vice President now constitutionally mandated to become acting President in the absence of Maduro. Trump also dismissed the possibility of the Nobel Prize-winning Machado leading the transition process, while failing to mention González, the Presidential candidate. This begs the question. What transition?

How has the global community reacted to these stunning developments? One does not need to be a legal expert to realize that the US military aggression in Venezuela that led to the abduction of Maduro and his wife is a brazen violation of international law and the UN charter. It also left at least 40 Venezuelans dead, including significant damage to private property and infrastructure. Yet, European leaders – supposedly the champions of international law and a rules-based global order have, once again, generally failed to acknowledge that in an unambiguous fashion. They are petrified to upset Trump and sought refuge in mealy-mouthed statements and carefully crafted obfuscation. Here are some notable examples, starting with the UK, which claims to enjoy a ‘special relationship’ with the USA.

Prime Minister Keir Starmer said the UK will discuss the “evolving situation” in Venezuela with U.S. counterparts while noting Britain will “shed no tears” about the demise of Maduro’s “regime”. This interview with Starmer from the British TV channel ITV is riveting to watch.

The EU expressed concern at the developments and urged respect for international law, even as it noted that Maduro “lacks legitimacy.”

French President Emmanuel Macron called for 2004 presidential candidate Edmundo Gonzalez Urrutia to lead a political transition. On the other hand, France said the U.S. operation undermined international law, and no solution to Venezuela’s crisis can be imposed externally.

German Chancellor Friedrich Merz said that Maduro had “led his country to ruin,” but called the U.S. action legally “complex.”

Italian Prime Minister Giorgia Meloni was the only major European leader to side with the U.S., arguing its military action in Venezuela was “legitimate” and “defensive.”

What about Canada? Well…

Prime Minister Mark Carney said on X that, “Canada has not recognized Maduro’s illegitimate regime since the 2018 electoral fraud. The Canadian government welcomes the opportunity now available to the Venezuelan people to access freedom, democracy, peace, and prosperity.”

He added, “True to its longstanding commitment to the rule of law, sovereignty, and human rights, Canada calls on all parties to respect international law. We support the sovereign right of the Venezuelan people to decide and build their own future in a peaceful and democratic society.”

These mild and conditional utterances by Western leaders on what is clearly a breach of international law contrast sharply with what China and Russia had to say.

China delivered a strongly worded message to the United States on Monday (5th January) at an “emergency” meeting of the UN Security Council, calling on Washington to abide by international law, end its illusion that it is the world’s police force and court, and immediately release Nicolas Maduro and his wife.

Russia’s United Nations ambassador Vasily Nebenzya denounced US actions in Venezuela and urged the immediate release of detained Venezuelan President Nicolás Maduro during a United Nations Security Council session in New York on Monday, January 5.

India, on the other hand, appeared to adopt the Western strategy of obfuscation. Thus:

Argentine President Javier Milei, Trump’s ideological soulmate, characterized (the USA) as supporting “democracy, the defense of life, freedom, and property.”

“On the other side,” …are those accomplices of a narco-terrorist and bloody dictatorship that has been a cancer for our region.”

Other right-wing leaders in South America similarly seized on Maduro’s ouster to declare their ideological affinity with Trump.

In Ecuador, conservative President Daniel Noboa issued a stern warning for all followers of Hugo Chávez, Maduro’s mentor and the founder of the Bolivarian revolution: “Your structure will completely collapse across the entire continent.”

In Chile, where a presidential election last month marked by fears over Venezuelan immigration brought down the leftist government, far-right President-elect José Antonio Kast hailed the U.S. raid as “great news for the region.”

Left-wing presidents in Latin America — including Brazil’s Luiz Inácio Lula da Silva, Mexico’s Claudia Sheinbaum, Chile’s Gabriel Boric, and Colombia’s Gustavo Petro — expressed grave concerns over what they saw as U.S. bullying.

Lula said the raid set “an extremely dangerous precedent.” Sheinbaum warned it “jeopardizes regional stability.” Boric said it “violated an essential pillar of international law.” Petro called it “aggression against the sovereignty of Venezuela and of Latin America.”

In sum, global reaction to Maduro’s abduction by the US has been quite diverse, but one is struck by the muted response of Europe and other leaders from the West. They will face a stern test if Trump follows through on his threat to invade Greenland and forcibly take it away from Denmark. Certainly, the Danish intelligence service, traditionally a close American ally within the framework of NATO, is so worried that it has officially designated the United States as a ‘security risk’.

{kind=link}