COVID-19 has left its malevolent imprint on a global scale; it has also motivated multiple agencies and institutions to create and disseminate innovate datasets that have enabled the international community to make sense of the evolution of the current pandemic and policy responses to it. Some, such as Johns Hopkins University, have set the pace in tracking both morbidity and mortality across the world engendered by COVID-19. Others, such as the IMF and ILO, have compiled country-level responses to ameliorate the economic and social consequences of this persistent global contagion.

IMF has developed a ‘policy tracker’ that highlights monetary and fiscal policy actions undertaken by governments across the world. The dataset is primarily textual in nature.

ILO has created a global ‘monitor’ that seeks to capture the labour market consequences of COVID-19. The ‘monitor’ also collates government responses at the national level that aim to ameliorate such consequences.

The Blavatnik School of Government (henceforth BSG) at the University of Oxford has created a comprehensive data analytic tool to highlight the fact that:

Governments are taking a wide range of measures in response to the COVID-19 outbreak. This tool aims to track and compare policy responses around the world, rigorously and consistently.

I have delved into BSG’s diverse and rich dataset to illuminate (1) the overall stringency of government response (2) economic relief provided to business and the broader community based on the latest available data (September 9, 2020) as they prevail across the world.

One advantage of the the BSG dataset (officially known as ‘Oxford COVID-19 Government Response Tracker’ or OxCGRT) is that it aggregates diverse information into simple numerical indices. Like all COVID-19 related datasets that are currently available, OxCGRT is dynamic in nature and is updated with considerable frequency.

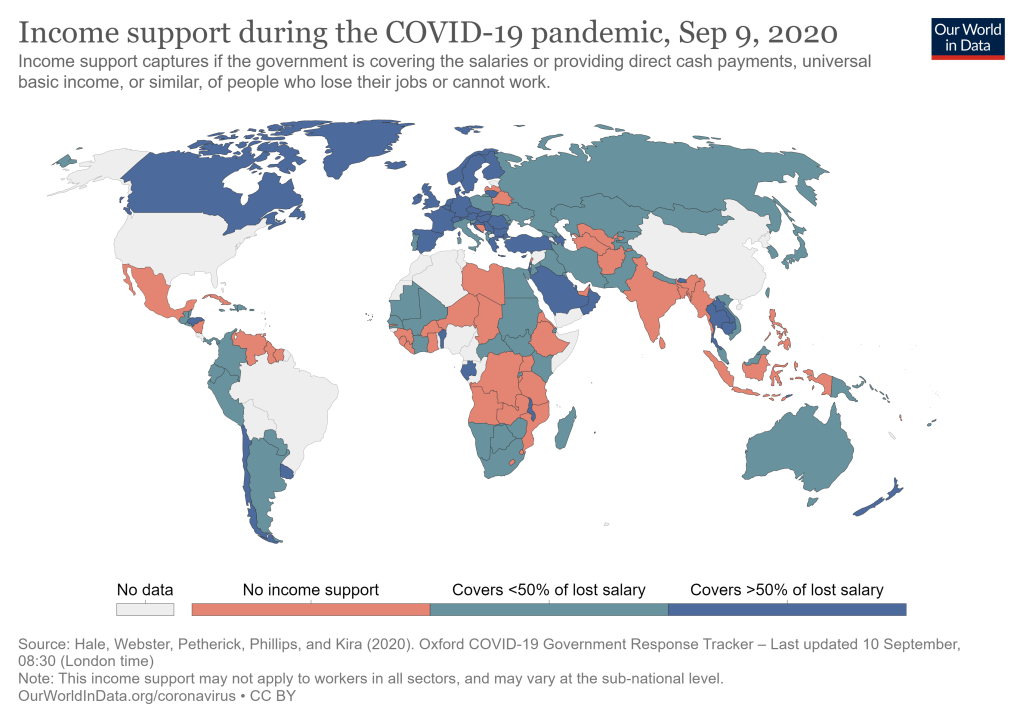

Shown below are a series of global maps that enable one to acquire a pictorial overview of country-level variations in government responses. In Map 1, one can detect the overall stringency of government response to COVID-19. This index is constructed from a variety of indicators, such as school and workplace closures. On a scale of 0-100 (100=strictest), countries generally vary from moderate (less than 50 as in Sri Lanka) to a high degree of stringency (above 70 as in parts of Australia).

Maps 2 and 3 focus on economic relief to business and the broader community. Such measures take two forms: (a) income support to targeted groups (b) debt or contract relief in which financial obligations (such as loan repayments) are temporarily suspended. Once again, there are notable variations in the generosity of economic support that is provided. Canada, for example, provides generous income support (defined as replacement of more than 50 percent of lost salary), while Australia does not. There are quite a few countries, including India, where there is no income support. In general, countries seem to have juxtaposed broad-based debt or contract relief with modest income support.

It has to be noted that, despite the strenuous efforts by a truly global team at BSG to compile diverse information in a user-friendly way on as many countries as possible (186 at last count), there are conspicuous examples of countries (Brazil and China) on which there are, as yet, no data, at least in this ‘mapped’ version. This is a source of concern and will act as a hurdle in deepening our understanding of how governments across the world are seeking to ameliorate the grave economic and social consequences of the current global pandemic.

Finally, as the team at BSG makes it amply clear, describing how governments have responded is only the beginning of the critical enterprise to evaluate how effective such responses have been. BSG has no doubt inspired many to undertake that next step.

MAPS OF THE WORLD ACCORDING TO BSG…